Chart of Accounts

Account Groups

SAP FINANCE

Bhupender Sharma

6/25/20253 min read

Chart of Accounts

By this time, we are aware of the Golden Rules and Types of Accounts. All of the previous Blogs were explaining basic concepts required for accounting.

Today, we know about the first object related to SAP directly, “Chart of Accounts”.

All the GLs (General Ledger) are structured systematically so that every user can remember and understand the purpose of each account created just by reading its Account number. Practically, the list may contain more than 1000 GLs depending on the company's line of Business.

Once the list is finalised, it is called “Chart of Accounts”. Depending on the ERP (Enterprise Resource Planning) software, the GLs can be created alphanumeric format, but generally, Numeric GL numbers are preferred.

Account Groups

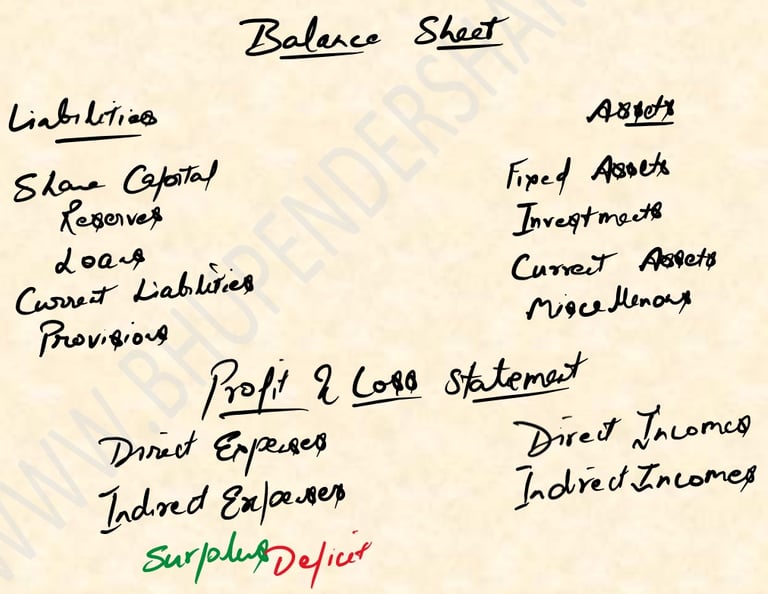

We have seen the structure of the Balance Sheet and the Profit and Loss statement

These categories are only a representation; practically, these can be different from company to company

The above categories are known as Account Groups in terms of SAP. We can say that these are Hierarchy levels defined within the Chart of Accounts.

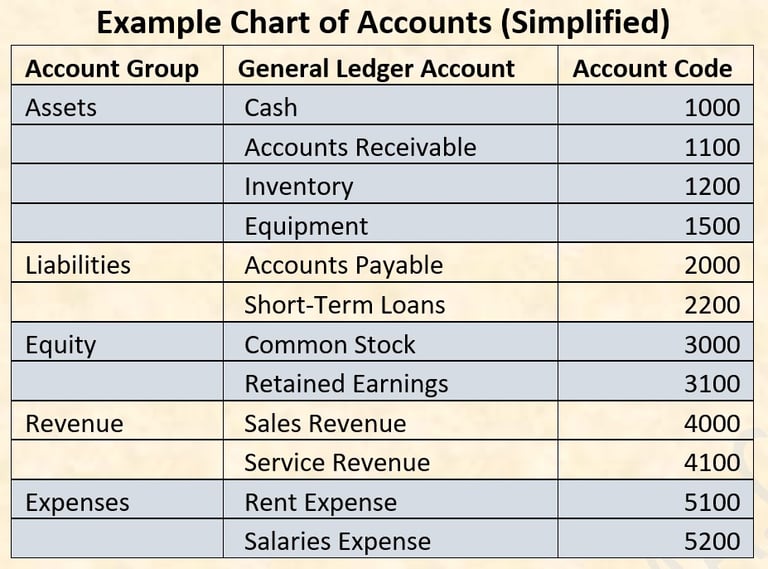

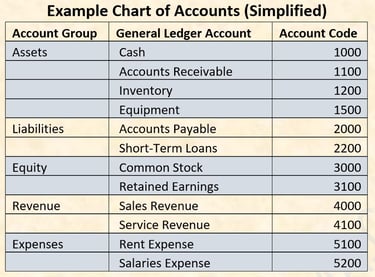

GLs are defined underneath these Account Groups. For ease of understanding, the Account Group codes and the GL numbers created within such Account groups are mostly created in parity.

If you observe the GL codes for Assets are starting with 1*, similarly Liabilities starts with 2*, Equity with 3*, Revenue with 4* and Expense with 5*.

In SAP GL Accounts codes can have a maximum length of 10 characters, while the Chart of Accounts and Account Group can have a maximum length of 4 characters, alpha-numeric.

Types of Chart of Accounts

Theoretically, 3 types of Chart of Accounts are known: -

Operating Chart of Accounts - Used for day-to-day accounting and financial transactions in a company code. Contains all G/L accounts required for operational accounting, such as revenue, expenses, assets, liabilities, and equity accounts.

Group Chart of Accounts - Used for consolidation and group-level reporting across multiple company codes within a corporate group. Each company code’s OCA accounts are mapped to GCA accounts for consolidated financial statements. Contains additional or modified G/L accounts required for local tax reporting, statutory financial statements, or other legal requirements.

Country Chart of Accounts - Addresses legal and statutory reporting requirements specific to a country. Contains alternative G/L accounts linked to the operating COA. Each operating G/L account can be assigned a country-specific account number for local reporting.

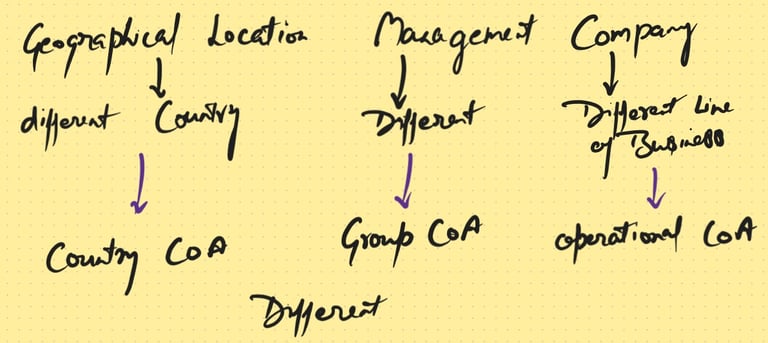

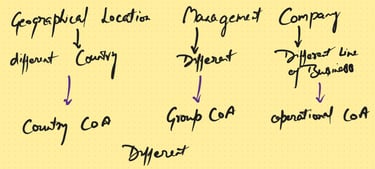

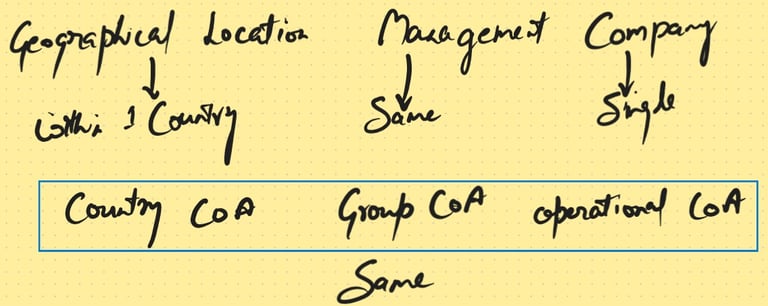

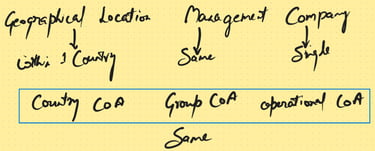

Conceptually, if a single company operates within one country under a unified management structure, the three types of Chart of Accounts are effectively identical. However, in practice, when a company operates across multiple countries or business lines with distinct managerial oversight, the three types diverge significantly in structure and function.

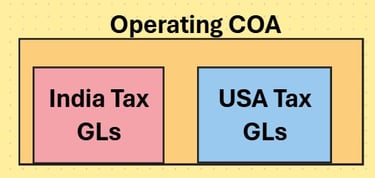

Country Chart of Accounts can be understood as sub set of Operating Chart of Accounts, where Operating COA caters to all the Geographical locations but consists of a few GLs that are particularly related to the laws of one or other country.

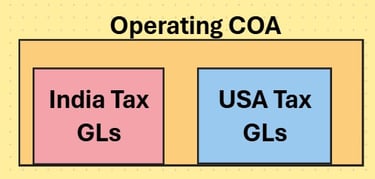

For example, GLs related to Tax, for India these shall be different while for USA the GL code would be different but part of the same Chart of Accounts. Same can be understood as below: -

From the image on the left, if we consider all GLs except Indian Tax GLs, then it shall be considered as the USA Country Chart of Accounts.

Similarly, if we consider all GLs except USA Tax GLs, then it shall be considered as the Indian Country Chart of Accounts.

I hope I have made the concept of COA a bit clearer and simpler for all of us.