Types of Accounts

Golden Rules of Accounting

SAP FINANCE

Bhupender Sharma

6/24/20253 min read

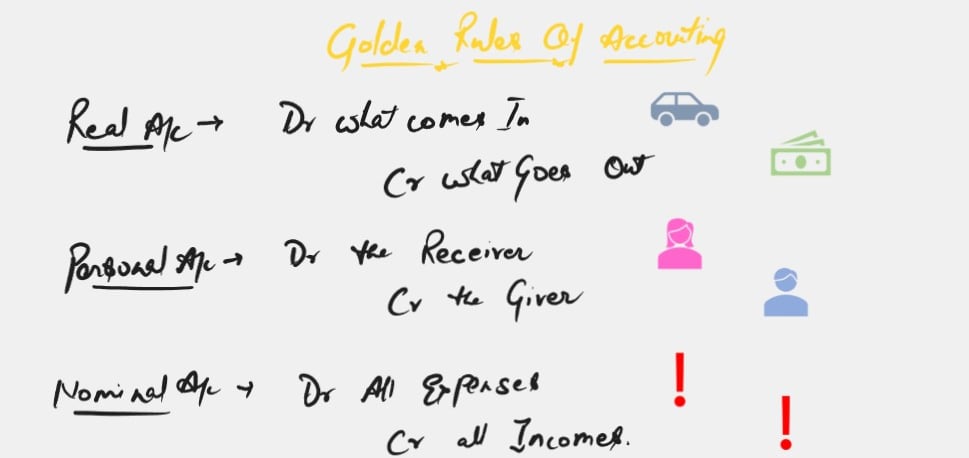

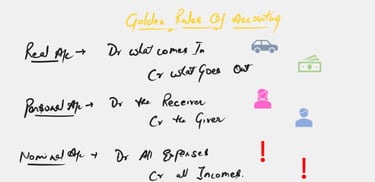

Golden Rules of Accounting-

Before explaining the concept of accounts, I believe we should revise the Golden Rules of Double Accounting, which are as follows: -

Real Account -

Debit what comes in,

Credit what goes out.

Personal Account -

Debit the receiver,

Credit the giver.

Nominal Account -

Debit all expenses

Credit all income.

The above rules imply that there will be something given or received against the other to complete the Financial transaction.

Now, most people get confused by these Rules, thinking that one type of account can only be posted with the same type of account, and thus, the rules were defined like that.

It takes most people about 3 to 4 years to understand that one type of Account can be posted with the same type of account as well as against another Type of account.

For example: -

If Real account is posted Dr. with Personal Account Cr., then the above Golden Rules shall be applied as below

Debit what comes in - Real Account

Credit the giver - Personal Account

Similarly, if Personal Account Dr. with Nominal account is posted Cr, then the above Golden Rules shall be as below

Debit the receiver - Personal Account

Credit tall income - Personal Account

If you have read till here, I believe you have understood the concept of Golden Rules, made so complicated by educational institutions so far. Let's try to understand the Types of accounts now.

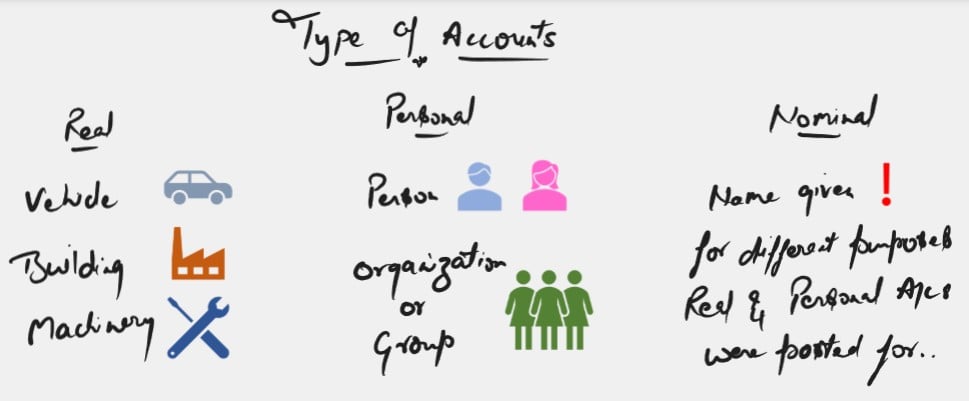

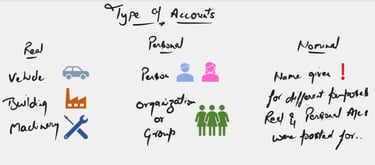

Types of Accounts-

Real Account - Normally, it is explained as suggested by the name, anything that can be felt physically shall be termed as Real Account. That statement is correct, but not complete in its manner.

For example: - Land, Building, Machinery, Furniture, Vehicle, Cash and Bank Balance are perfectly fitting as per the above definition. However, Copyrights, Lease deeds for property, and intangible assets, though created and treated as per the rules for Real Account but do not fit in the definition above.

Therefore, I would like to modify the definition as anything for which the right to use is similar to an owner for a term of more than a financial period shall be a Real Account.

Personal Account - The accounts for any person, organisation, firm or body representing a group of persons are defined as Personal Account.

Nominal Account - As per popular definition, "Any other account which is not Real or Personal Account is termed as Nominal Account to track revenue and expenses for a specific period". But I find Nominal Account as accounts in disguise, which are fillers for Real or Personal account to complete the Double Accounting Principle...

WHY! Let's find it...

I will try to explain it with an example of Salary Expenses (Nominal Account) incurred by any organisation. Whenever any organisation incurs Salary Expenditure following posting is booked:-

Salary Expenses Debit - Nominal Account

Cash or Bank Balance Credit - Real Account

What happening here in reality is that only the Cash / Bank Balance is going out and is posted in Credit, but nothing is received against that, therefore A name "Salary" is been used for which the cash/bank balance has gone out.

If we carefully examine other transactions related to different expenses or incomes, most of the time it is the cash/bank balance that has gone out or been received in. To differentiate the purpose of payments or receipts, different names are assigned, and that's how the double accounting principle is adhered.

For reference, Loan given, Interest Charged, Penalty Paid, Sales Revenue received, Royalty paid, Rental income received and so on. In all the references, Cash/Bank Balance is either going out or coming in for different purposes identified with different Nominal Accounts.

The same applies for Personal accounts posted against Nominal Accounts that you owe from or to another person some amount for differentiated purposes identified as Nominal Account.